For my purchases and sales

Secure your transactions between individuals on all your usual sites.

March 8, 2024

You've come to the right place if you're looking for which payment service provider to integrate into your Swiss marketplace. In this article, we provide you with the keys to understanding the different technical options available to you, their advantages and disadvantages, what is the applicable legal framework and which are the main players operating in Switzerland.

You can also read our article on how to easily integrate Swiss Post into its Swiss marketplace.

The market for transactions between private individuals and second-hand vehicles in Switzerland is growing strongly, driven by the ecological considerations of citizens and the desire to preserve purchasing power. This explains the emergence of a large number of generalist and specialized platforms.

The global market is now worth more than €128 billion and is growing at a compound annual rate of +22% (See the full market study from Tripartie).

Disclaimer: This fact sheet was written by the team Tripartie with the aim of clarifying the legal framework applicable to the payment functionality on a Swiss marketplace, as well as the obligations and risks arising from it, for all stakeholders. It is in no way a substitute for the advice of a legal professional and does not constitute any recommendation.

If you want to monetize your Swiss marketplace by taking a commission and manage paid transactions, you must comply with the applicable legislation and in particular the banking monopoly.

What is commonly referred to as the "banking monopoly" is the prohibition on any person other than certain categories of authorised entities from carrying out banking transactions regularly.

The European Union directives define the concept of a credit institution as "an undertaking whose activity consists in receiving deposits or other repayable funds from the public and in granting credit on its own account".

Swiss financial market laws stipulate that the Swiss Financial Market Supervisory Authority (FINMA, from Germany's Eidgenössische Finanzmarktaufsicht, which partly takes over the responsibilities of the Swiss Federal Banking Commission, which was dissolved on 1 January 2009) must first authorise the exercise of certain business activities. Thus, "anyone who accepts deposits of more than 20 people or advertises such an activity in principle needs a prior banking licence from FINMA".

Since 1 January 2019 in Switzerland, anyone who accepts deposits from the public up to CHF 100 million on a professional basis or calls on the public to obtain them and does not invest or remunerate these deposits is no longer considered a bank. For establishments of this nature, a Fintech authorisation is provided, the obtaining of which is subject to lighter requirements.

FINMA "intervenes against such activities carried out without right by applying the laws on the financial markets: on the basis of the specific information in its possession, it carries out in-depth investigations if necessary, which, if the suspicions are confirmed, can lead to enforcement proceedings and concrete measures" (source: finma.ch).

It is therefore illegal to manually manage payments on behalf of users of your Swiss marketplace, without prior authorization. Obtaining such authorization is expensive and requires expertise, which is why platforms use a dedicated payment service provider.

A payment service provider (PSP) is a company that enables online platforms to accept payments from their users. The PSP acts as the link between the means of payment (credit card, bank transfer, etc.) and the platform, providing the latter with the solutions needed to integrate and manage payments in full compliance.

The payment service provider is also responsible for fraud prevention, protecting sensitive data related to your users' payment methods and identity, verifying identity, and maintaining legal compliance.

Usually, the first criterion we look at when selecting a payment service provider is pricing. Payment is often seen as a convenience, one wants it to work properly and both pay for it as cheaply as possible.

Beyond the price, it is important to compare the countries, payment methods and currencies supported by the payment service provider, to ensure that they are in line with the objectives of its Swiss marketplace. Will I carry out cross-border transactions? Will I internationalize my platform in the medium term?

Finally, the simplicity of integration, the performance of the integrated features (anti-fraud detection or KYC management for example) or reputation must be taken into account.

Now that we've explained why a payment service provider is a must-have on your Swiss marketplace, let's take a look at the two possible integration options.

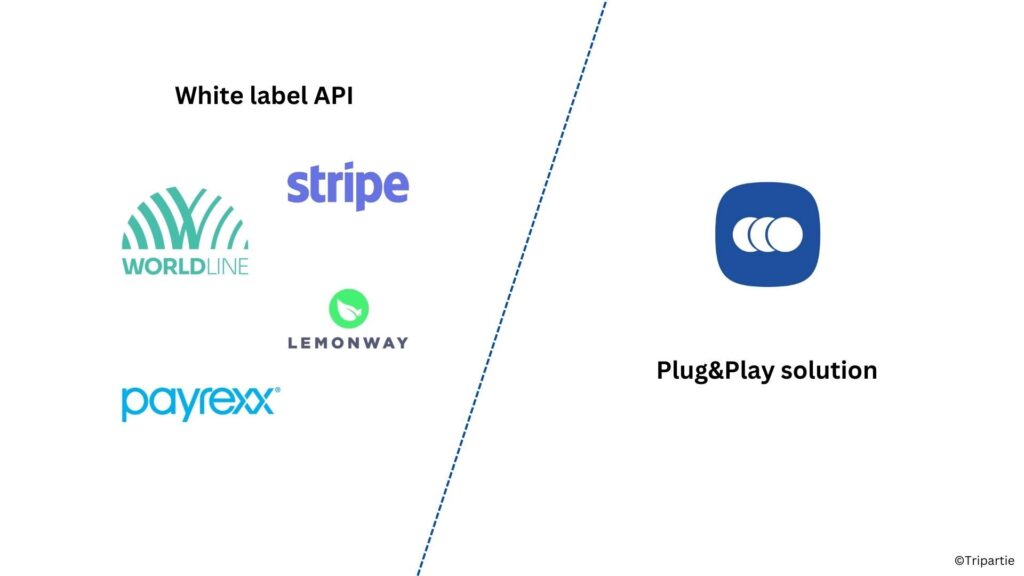

| Option 1: Traditional white-label API integration | Option n°2: The integration of a Plug & Play solution (SaaS mode) |

| Advantage: You have complete control over the user experience and there is no mention of the payment service provider on your platform. | Benefits: The administrative activation of your account is instantaneous as soon as the contract is signed. User journeys are already integrated and ready to use. Technical integration is done in a few hours of work, which drastically reduces your IT development budget and lightens your product roadmap. The day-to-day tracking of transactions is done automatically, so you can focus on what really matters. |

| Disadvantages: The deployment takes a long time: minimum 6 months to compile your company's administrative file and have it validated by the payment service provider. All user journeys are to be developed by yourself, which requires a very strong involvement of your team. The costs associated with course development and technical integration are high. This type of integration involves monitoring the smooth running of payments on a daily basis via the payment service provider's dashboard. | Disadvantage: although the paths are generally configurable and in your colors, you do not fully control the user experience. |

At Tripartie, we are all about simplification and believe that your resources should be focused on building an offer, acquiring and creating an exceptional buying and selling experience. We therefore recommend the integration of a Plug&Play solution due to its speed and savings.

There are dozens of payment service providers in Europe, and a few web searches make it easy to identify them. Below, we show a few examples that we feel are relevant to the launch of a Swiss marketplace. In fact, not all service providers offer dedicated services for marketplaces. Sometimes, the payment service provider specialises solely in BtoC e-commerce sites or payments in physical stores.

Teorem is an application for buying and selling fashion items between private individuals operating in Switzerland. Launched by a fashion and second-hand enthusiast, Teorem quickly established itself as a benchmark. Today, the application enables users not only to create sales areas for clothing and accessories but also to hunt for bargains in the community's dressing rooms.

In 2020, while Vinted and other players in the sale of fashion items between individuals are expanding around the world, no solution exists for the inhabitants of Switzerland, a blockage due to the different legislations. It was in this context that Teorem was born.

With the mission to encourage more responsible and sustainable fashion consumption as well as to bring together second-hand enthusiasts, Teorem has more than 30,000 active users.

The security of transactions is a central issue since Teorem operates in a market where fraudsters do not fail to innovate and where the degree of satisfaction is not the same between two users, sometimes leading to disputes between them.

In its early days, the app only offered a service to connect individuals. The Teorem team then wanted to integrate secure payment to monetise exchanges.

How did Tripartie help Teorem achieve its goals?

Thanks to its unique technical and contractual architecture, Tripartie has made it possible for:

Tripartie allows you to invest in the second-hand market and transactions between individuals quickly, without operational and reputational risk. Our differentiation: Plug & Play solutions based on trust, integrating a payment service provider and allowing you to manage all transactions in your Swiss marketplace.

The Safe Checkout solution from Tripartie is a secure payment button accessible in SaaS mode that makes your platform's entire online purchasing chain more reliable:

The team Tripartie has thought of everything for Swiss marketplaces :

Launching a Swiss marketplace? Book a product demo!

Toolkit

Toolkit

C2C platforms, find out how the Resolution Center can automate your marketplace's dispute handling.

Find out more